OneSource Specialty Pharma: A capacity-led bet on the GLP-1 gold rush

OneSource Specialty Pharma is emerging as a surprising beneficiary of the global GLP-1 boom. With semaglutide patents set to expire across key markets and demand for injection pens surging, the Bengaluru-based CDMO is scaling aggressively for what could become a multi-year manufacturing opportunity.

There is a manufacturing facility in Bengaluru that most investors have never heard of.

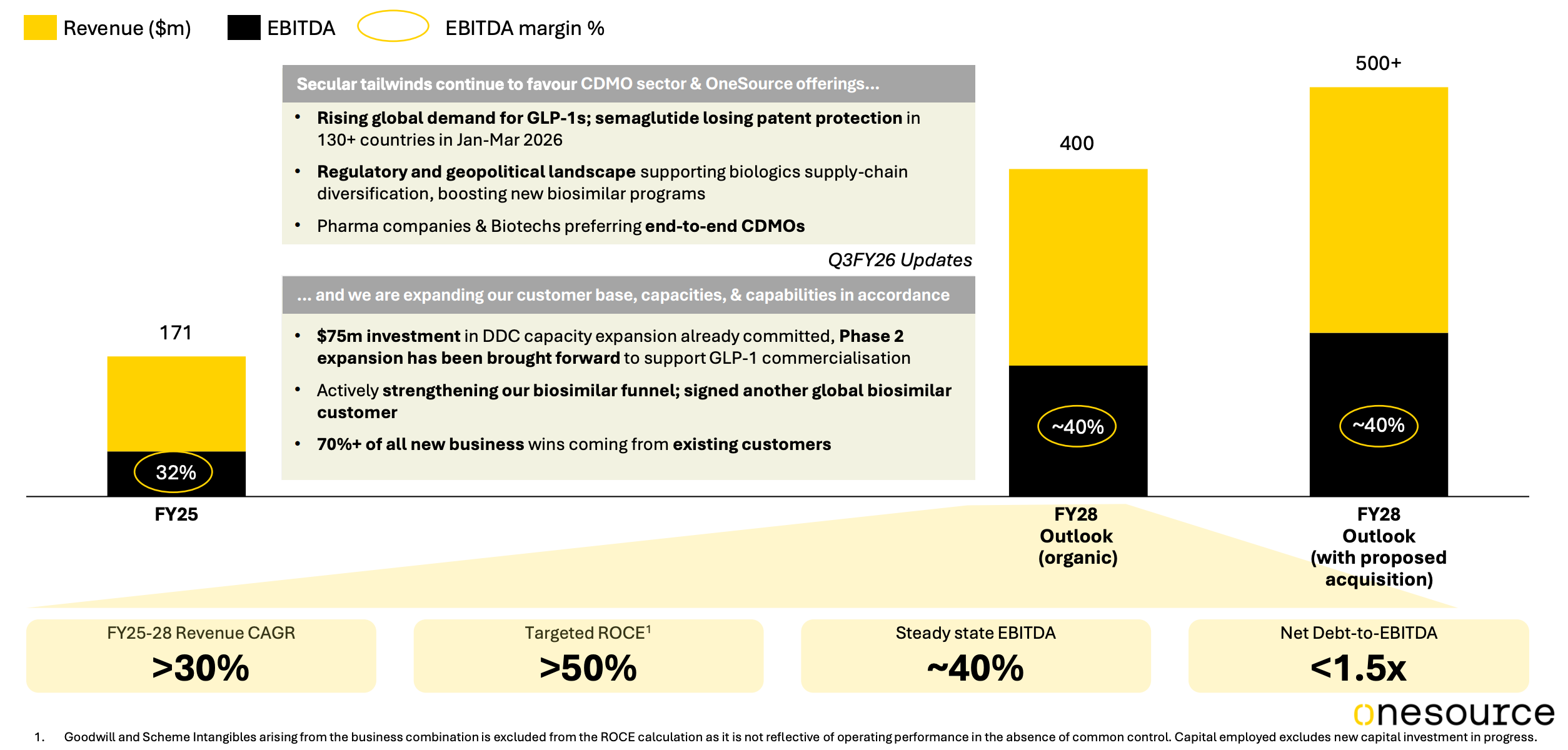

From revenue of $170 million in FY25, the company is guiding for $500 million by FY28 with EBITDA margins of 40%.

That implies nearly 3x growth in three years, alongside an 800-basis-point margin expansion. And all of it is tied to what may be the single biggest pharmaceutical patent cliff of this decade.

Yet for most of the 15 months since its demerger from Strides Pharma, almost nobody was paying attention.

That has started to change.

Source: http://www.tradingview.com

The reason OneSource Specialty Pharma is suddenly impossible to ignore is not because the business transformed overnight. It is because three powerful trends are converging simultaneously: the explosive growth of the GLP-1 market, the patent cliff for semaglutide, and the global shift toward high-complexity contract manufacturing.

Demand is no longer the question. The only real variable is the timing of regulatory approvals. And on April 21, 2026, that variable moved sharply in the company’s favour.

Understanding what OneSource builds

OneSource Specialty Pharma was demerged from Strides Pharma in 2024 and listed separately in January 2025. The company officially reports revenue under a single segment: CDMO (Contract Development and Manufacturing Organisation).

Within CDMO, however, the business operates across three key sub-segments, though the exact revenue split is not disclosed in investor presentations or the FY25 annual report. These sub-segments include:

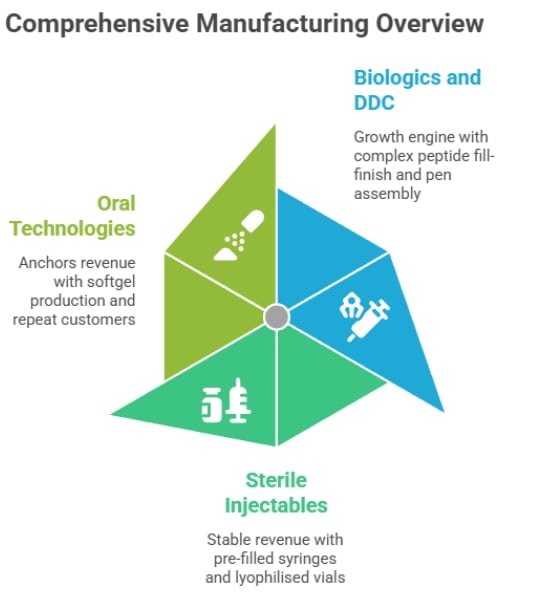

Drug-Device Combinations (DDC) and Biologics: Growth Engine

Drug-Device Combinations is the company’s primary growth engine. The segment is already scaling rapidly, driven by strong demand for GLP-1 therapies.

Ongoing capex will expand cartridge capacity from roughly 40 million units in FY25 to 220 million units by the end of FY27. This expansion is backed by long-term supply agreements, many of which include upfront capacity reservation fees from more than 20 GLP-1 customers, including four of the top five global generic players.

Under the DDC segment, OneSource manufactures GLP-1 injection pens, not generic injectable drugs or tablets. These are sophisticated delivery systems that require years of comparability studies, device validation, and human-factor testing before regulatory approval.

Source: OneSource Website

Once regulators validate a manufacturing site for a specific process, switching suppliers becomes operationally complex and commercially unattractive.

The company’s Bengaluru flagship facility is already USFDA-approved for biologics fill-finish and device assembly*, a capability very few Indian plants possess.

The company’s flagship Bengaluru facility is already USFDA-approved for biologics fill-finish and device assembly, capabilities that very few Indian facilities possess.

Fill-finish refers to the final stage of sterile manufacturing, where purified biologic drugs are filled into vials or syringes and assembled into ready-to-use injection devices.

Sterile injectables: Stable high-value base

Sterile injectables, including complex formulations, pre-filled syringes, and lyophilized vials, form a substantial and stable part of the business. The company serves customers across the US, Europe, and Australia.

High regulatory barriers protect the segment from commodity-style pricing pressure, enabling relatively stable growth. It is expected to deliver steady growth supported by capacity expansions (e.g., scaling pre-filled syringes) and new product introductions.

Softgel (Oral Technologies): Steady ofundation

Softgel manufacturing remains the company’s steady foundation.

With an annual capacity of 2.4 billion capsules, OneSource ranks among the top five global softgel CDMO players. While the segment’s relative contribution may decline as faster-growing businesses such as DDC scale up, the underlying business remains strong and continues to benefit from consistent demand and operational efficiencies.

As noted earlier, the company does not disclose revenue contribution by sub-segment.

Financials

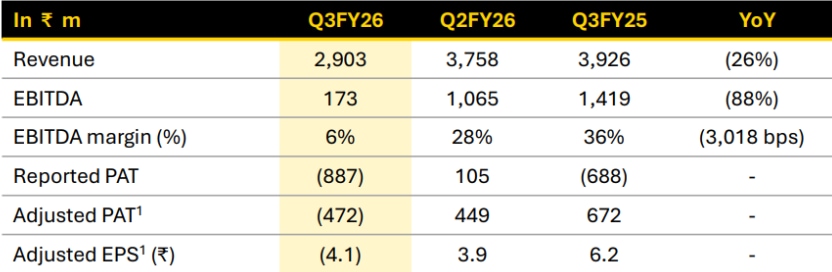

At first glance, Q3FY26 appears weak.

Revenue declined 26% YoY to Rs 290 crore, EBITDA margins fell sharply from 36% to 6%, and adjusted PAT turned negative.

Source: OneSource Q3 FY26 Investors Presentation

But context matters.

FY25 benefited from milestone-linked CDMO income, creating a high base for comparison. Management also indicated that capacity allocation remained focused on upcoming GLP-1 commercial opportunities, while regulatory delays in Canada for a key semaglutide programme pushed back planned deliveries.

Importantly, management maintained that underlying demand trends remain intact:

So while quarterly numbers were weak, management commentary suggests the issue was primarily one of timing and utilisation rather than a collapse in demand.

What is even more encouraging is that RFPs (Request for Proposal) continue to trend upwards, and the company has onboarded another global biosimilar player in the biologics segment. The inherent demand remains intact.

The GLP-1 opportunity is only beginning

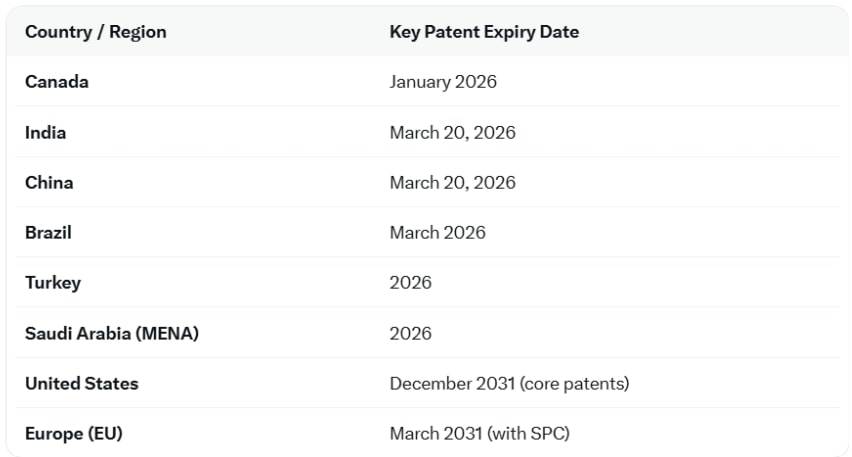

GLP-1 receptor agonists such as semaglutide and tirzepatide generated more than $67 billion in global sales during calendar year 2025. What makes the opportunity even larger is the approaching patent expiry cycle. Semaglutide patents begin expiring from 2026 onward across Canada, Brazil, China, India, and eventually broader global markets.

GLP-1 receptor agonists mimic the body’s natural “fullness hormone,” helping lower blood sugar, suppress appetite, and drive significant weight loss.

Source: Author research

This creates a manufacturing opportunity estimated at 500 million to 1 billion additional pen devices annually, equivalent to a $1-2 billion addressable market for CDMOs.

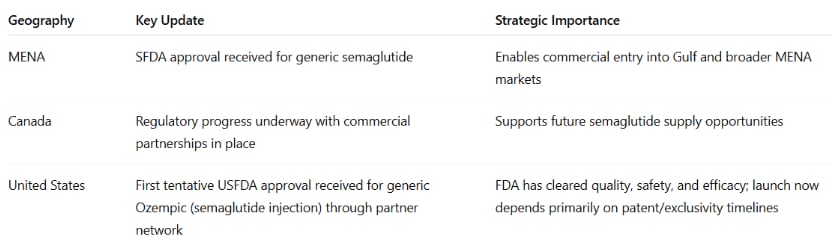

OneSource has already secured multiple regulatory and commercial milestones across key semaglutide markets.

Source: Investor presentations & Company con-calls

Tentative FDA approval is particularly significant. It means the product has already cleared quality, safety, and efficacy requirements. The remaining hurdle is patent and exclusivity clearance before commercial launch.

At this stage, the bottleneck appears less about demand and more about how quickly approvals translate into commercial supply volumes.

Capex and operating leverage: The inflection is here

Management’s FY28 guidance remains firm: $500 million in revenue, 40 percent EBITDA margins in steady state, and net debt to EBITDA below 1.5x.

The math behind that target is straightforward.

More than $100 million in capex is being deployed over four years to expand DDC cartridge capacity from 40 million to 220 million units, scale pre-filled syringe lines, and build supporting infrastructure. Most of this investment is already committed, with the expanded capacity expected to become fully operational by FY27.

This is the classic setup for operating leverage. Fixed costs are being locked in today. If multiple high-margin GLP-1 programmes fire simultaneously across MENA, Canada, and the US, the same cost base spreads across a materially larger revenue base.

The result is non-linear margin expansion, The next 24 months will revolve around two parallel developments: completing the capacity build-out and converting regulatory approvals into commercial supply. Both are already underway. The question is purely one of timing.

Source: OneSource Q3FY26 Investors presentation

Risks

No investment case is complete without an honest accounting of what could go wrong.

Valuations: Where the asymmetry lives

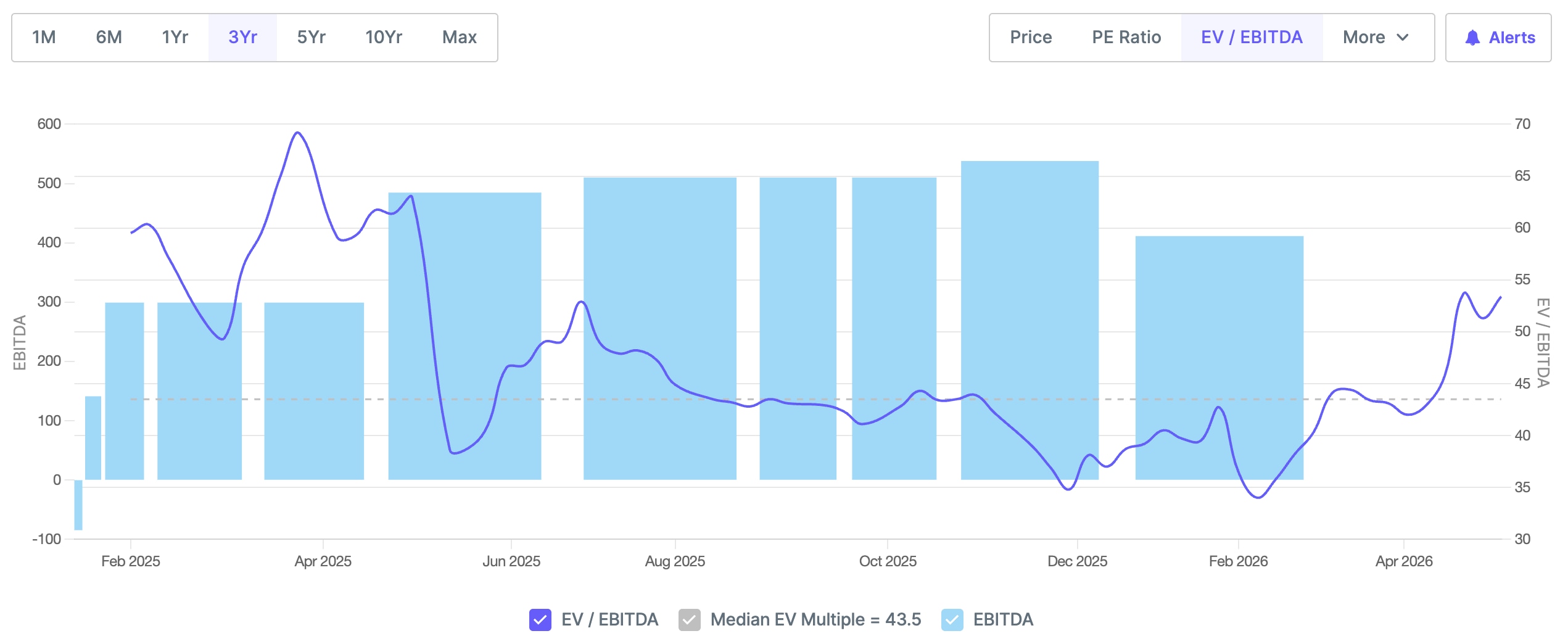

Trailing valuations appear expensive at first glance. With a market capitalisation of roughly Rs 20,000 crore and a current revenue run rate of Rs 1,400 crore, the trailing EV/EBITDA sits above 50x. That number alone will likely deter many investors.

Source: http://www.screener.in

But trailing multiples may be the wrong lens for a business poised for growth.

Under FY28 guidance, the picture changes dramatically.

Rs 4,200 crore revenue at 40% EBITDA margins would imply roughly Rs 1,680 crore EBITDA, equivalent to nearly 12x forward EV/EBITDA for a business capable of generating high-teen to 20%+ ROCE once utilisation normalises.

The asymmetry is simple. Most investors chasing the GLP-1 wave are buying Novo Nordisk and Eli Lilly at peak valuations, with the best already priced in. OneSource sits one step behind in the value chain, manufacturing the generic version of the same drugs at a fraction of the cost, with the approval catalysts still ahead of it.

The growth in the next 3-5 years may well be in the companies that actually make the affordable versions at scale.

OneSource has built the plant, secured the approvals, and locked in the partners. The next 24 months are pure execution and operating leverage, exactly the kind of setup that creates asymmetric returns in specialty pharma. The hard part is already done. The other part, scaling into a multi-billion-dollar tailwind, is just beginning.

The moat appears durable, the demand is secular, and the timing just got a whole lot better.

In the GLP-1 gold rush, the quiet manufacturers who own the pens may end up with more durable alpha than the brands themselves. OneSource is positioning itself squarely in that camp.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

There is a manufacturing facility in Bengaluru that most investors have never heard of.

From revenue of $170 million in FY25, the company is guiding for $500 million by FY28 with EBITDA margins of 40%.

That implies nearly 3x growth in three years, alongside an 800-basis-point margin expansion. And all of it is tied to what may be the single biggest pharmaceutical patent cliff of this decade.

Yet for most of the 15 months since its demerger from Strides Pharma, almost nobody was paying attention.

That has started to change.

Source: http://www.tradingview.com

The reason OneSource Specialty Pharma is suddenly impossible to ignore is not because the business transformed overnight. It is because three powerful trends are converging simultaneously: the explosive growth of the GLP-1 market, the patent cliff for semaglutide, and the global shift toward high-complexity contract manufacturing.

Demand is no longer the question. The only real variable is the timing of regulatory approvals. And on April 21, 2026, that variable moved sharply in the company’s favour.

Understanding what OneSource builds

OneSource Specialty Pharma was demerged from Strides Pharma in 2024 and listed separately in January 2025. The company officially reports revenue under a single segment: CDMO (Contract Development and Manufacturing Organisation).

Within CDMO, however, the business operates across three key sub-segments, though the exact revenue split is not disclosed in investor presentations or the FY25 annual report. These sub-segments include:

Drug-Device Combinations (DDC) and Biologics: Growth Engine

Drug-Device Combinations is the company’s primary growth engine. The segment is already scaling rapidly, driven by strong demand for GLP-1 therapies.

Ongoing capex will expand cartridge capacity from roughly 40 million units in FY25 to 220 million units by the end of FY27. This expansion is backed by long-term supply agreements, many of which include upfront capacity reservation fees from more than 20 GLP-1 customers, including four of the top five global generic players.

Under the DDC segment, OneSource manufactures GLP-1 injection pens, not generic injectable drugs or tablets. These are sophisticated delivery systems that require years of comparability studies, device validation, and human-factor testing before regulatory approval.

Source: OneSource Website

Once regulators validate a manufacturing site for a specific process, switching suppliers becomes operationally complex and commercially unattractive.

The company’s Bengaluru flagship facility is already USFDA-approved for biologics fill-finish and device assembly*, a capability very few Indian plants possess.

The company’s flagship Bengaluru facility is already USFDA-approved for biologics fill-finish and device assembly, capabilities that very few Indian facilities possess.

Fill-finish refers to the final stage of sterile manufacturing, where purified biologic drugs are filled into vials or syringes and assembled into ready-to-use injection devices.

Sterile injectables: Stable high-value base

Sterile injectables, including complex formulations, pre-filled syringes, and lyophilized vials, form a substantial and stable part of the business. The company serves customers across the US, Europe, and Australia.

High regulatory barriers protect the segment from commodity-style pricing pressure, enabling relatively stable growth. It is expected to deliver steady growth supported by capacity expansions (e.g., scaling pre-filled syringes) and new product introductions.

Softgel (Oral Technologies): Steady ofundation

Softgel manufacturing remains the company’s steady foundation.

With an annual capacity of 2.4 billion capsules, OneSource ranks among the top five global softgel CDMO players. While the segment’s relative contribution may decline as faster-growing businesses such as DDC scale up, the underlying business remains strong and continues to benefit from consistent demand and operational efficiencies.

As noted earlier, the company does not disclose revenue contribution by sub-segment.

Financials

At first glance, Q3FY26 appears weak.

Revenue declined 26% YoY to Rs 290 crore, EBITDA margins fell sharply from 36% to 6%, and adjusted PAT turned negative.

Source: OneSource Q3 FY26 Investors Presentation

But context matters.

FY25 benefited from milestone-linked CDMO income, creating a high base for comparison. Management also indicated that capacity allocation remained focused on upcoming GLP-1 commercial opportunities, while regulatory delays in Canada for a key semaglutide programme pushed back planned deliveries.

Importantly, management maintained that underlying demand trends remain intact:

So while quarterly numbers were weak, management commentary suggests the issue was primarily one of timing and utilisation rather than a collapse in demand.

What is even more encouraging is that RFPs (Request for Proposal) continue to trend upwards, and the company has onboarded another global biosimilar player in the biologics segment. The inherent demand remains intact.

The GLP-1 opportunity is only beginning

GLP-1 receptor agonists such as semaglutide and tirzepatide generated more than $67 billion in global sales during calendar year 2025. What makes the opportunity even larger is the approaching patent expiry cycle. Semaglutide patents begin expiring from 2026 onward across Canada, Brazil, China, India, and eventually broader global markets.

GLP-1 receptor agonists mimic the body’s natural “fullness hormone,” helping lower blood sugar, suppress appetite, and drive significant weight loss.

Source: Author research

This creates a manufacturing opportunity estimated at 500 million to 1 billion additional pen devices annually, equivalent to a $1-2 billion addressable market for CDMOs.

OneSource has already secured multiple regulatory and commercial milestones across key semaglutide markets.

Source: Investor presentations & Company con-calls

Tentative FDA approval is particularly significant. It means the product has already cleared quality, safety, and efficacy requirements. The remaining hurdle is patent and exclusivity clearance before commercial launch.

At this stage, the bottleneck appears less about demand and more about how quickly approvals translate into commercial supply volumes.

Capex and operating leverage: The inflection is here

Management’s FY28 guidance remains firm: $500 million in revenue, 40 percent EBITDA margins in steady state, and net debt to EBITDA below 1.5x.

The math behind that target is straightforward.

More than $100 million in capex is being deployed over four years to expand DDC cartridge capacity from 40 million to 220 million units, scale pre-filled syringe lines, and build supporting infrastructure. Most of this investment is already committed, with the expanded capacity expected to become fully operational by FY27.

This is the classic setup for operating leverage. Fixed costs are being locked in today. If multiple high-margin GLP-1 programmes fire simultaneously across MENA, Canada, and the US, the same cost base spreads across a materially larger revenue base.

The result is non-linear margin expansion, The next 24 months will revolve around two parallel developments: completing the capacity build-out and converting regulatory approvals into commercial supply. Both are already underway. The question is purely one of timing.

Source: OneSource Q3FY26 Investors presentation

Risks

No investment case is complete without an honest accounting of what could go wrong.

Valuations: Where the asymmetry lives

Trailing valuations appear expensive at first glance. With a market capitalisation of roughly Rs 20,000 crore and a current revenue run rate of Rs 1,400 crore, the trailing EV/EBITDA sits above 50x. That number alone will likely deter many investors.

Source: http://www.screener.in

But trailing multiples may be the wrong lens for a business poised for growth.

Under FY28 guidance, the picture changes dramatically.

Rs 4,200 crore revenue at 40% EBITDA margins would imply roughly Rs 1,680 crore EBITDA, equivalent to nearly 12x forward EV/EBITDA for a business capable of generating high-teen to 20%+ ROCE once utilisation normalises.

The asymmetry is simple. Most investors chasing the GLP-1 wave are buying Novo Nordisk and Eli Lilly at peak valuations, with the best already priced in. OneSource sits one step behind in the value chain, manufacturing the generic version of the same drugs at a fraction of the cost, with the approval catalysts still ahead of it.

The growth in the next 3-5 years may well be in the companies that actually make the affordable versions at scale.

OneSource has built the plant, secured the approvals, and locked in the partners. The next 24 months are pure execution and operating leverage, exactly the kind of setup that creates asymmetric returns in specialty pharma. The hard part is already done. The other part, scaling into a multi-billion-dollar tailwind, is just beginning.

The moat appears durable, the demand is secular, and the timing just got a whole lot better.

In the GLP-1 gold rush, the quiet manufacturers who own the pens may end up with more durable alpha than the brands themselves. OneSource is positioning itself squarely in that camp.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.