Inside Adani Green’s high-leverage bet on India’s 500 GW energy transition

Adani Green Energy added more renewable capacity in FY26 than any company outside China, accounting for nearly 9% of India’s total clean energy additions. But behind the record growth lies transmission bottlenecks, Rs 1,500 crore of voluntarily sacrificed EBITDA, rising debt, and an aggressive battery storage push that could define the next phase of India’s energy transition.

In FY26, Adani Green Energy Limited (AGEL) added 5,051 megawatts (MW) of renewable energy capacity, the largest greenfield renewable addition by any company outside China.

During the same period, India added 55 gigawatts (GW), or 55,000 MW, of non-fossil fuel capacity, marking the country’s best year on record. This includes solar, wind, biomass, and both small and large hydro projects.

That means AGEL alone accounted for roughly 9% of India’s total renewable capacity additions and nearly 14% of the country’s solar and wind additions.

With India’s installed non-fossil base now at 283 GW and the official target set at 500 GW by 2030, the country must add another 50-55 GW annually over the next five years. AGEL is currently the single largest contributor to that expansion.

Source: http://www.tradingview.com

This explains why the stock has been rallying.

To understand AGEL’s long-term outlook, three questions matter:

The pace of green energy addition

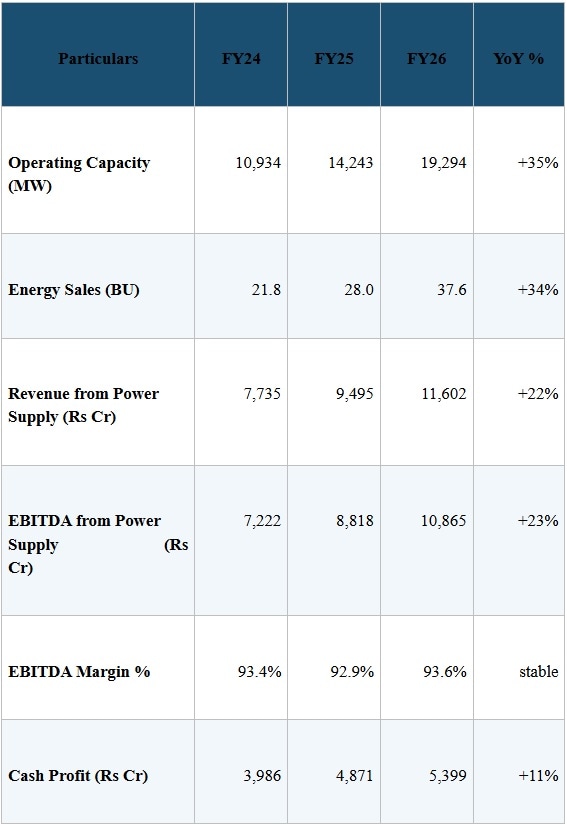

AGEL ended FY26 with 19.3 GW of operating renewable capacity, up from 14.2 GW a year earlier. The 35% year-on-year growth extends a five-year capacity CAGR of 42%.

In terms of units of power sold, energy sales reached 37.6 billion units (BU), up 34% YoY, roughly equivalent, according to AGEL, to Denmark’s annual electricity consumption.

Source: AGEL FY25 Annual Report 5-year KPI table; AGEL Q4 FY26 Investor Presentation

However, the composition of that growth matters.

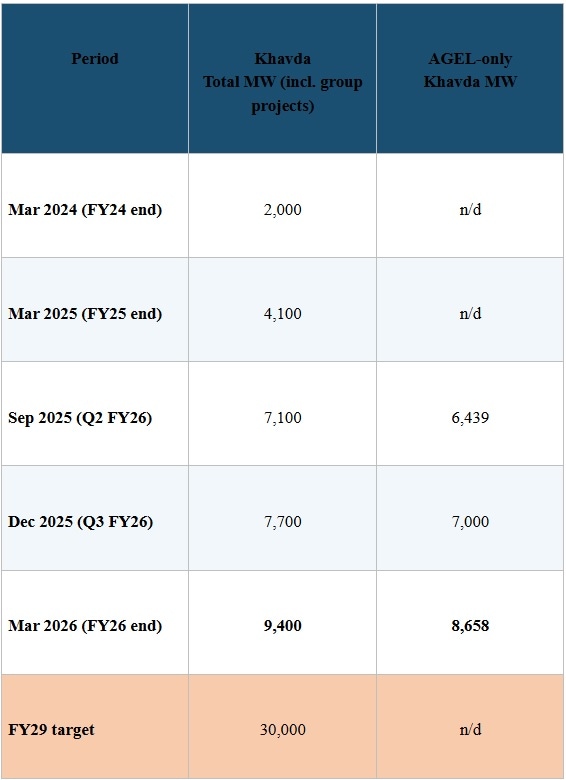

Of the 5,051 MW added in FY26, 4,613 MW came from a single site — Khavda. Another 438 MW came from Rajasthan, while Andhra Pradesh contributed the remainder.

In effect, one mega-project is driving the company’s growth trajectory, with every other site playing a supporting role.

The Khavda engine

Khavda, a 538-square-kilometre stretch of wasteland in the Rann of Kutch, had no operating capacity just two years ago.

Today, it hosts 9.4 GW of solar, wind, and hybrid projects, along with 1,376 megawatt-hours (MWh) of battery storage capacity. In FY26 alone, Khavda contributed 5.3 GW of AGEL’s total capacity addition. The target is 30GW by FY29.

Source: AGEL FY25 Annual Report; Investor presentations

AGEL’s execution strategy at Khavda rests on three pillars:

One detail often overlooked is that AGEL’s internal capability is 7-8 GW of capacity addition per year. Management is throttling delivery to 4.5-5 GW because the transmission grid downstream cannot evacuate any faster.

In FY27, another 14-15 GW of evacuation capacity is expected to come online at Khavda. If that lands on schedule, AGEL’s pace of execution could accelerate significantly. But scaling this quickly has unintended consequences.

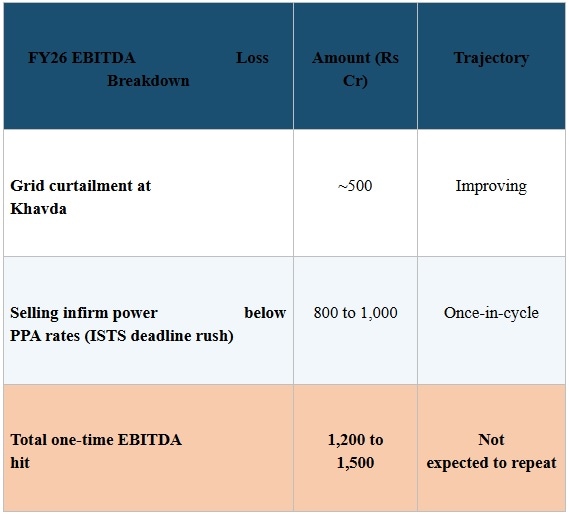

In FY26, those consequences showed up as roughly Rs 1,500 crore of foregone EBITDA.

Why AGEL left Rs 1,500 crore voluntarily on the table

During its Q4 FY26 earnings call, AGEL disclosed that it sacrificed between Rs 1,200 crore and Rs 1,500 crore of EBITDA during the year.

The loss came from two sources.

First, around Rs 500 crore was lost due to grid curtailment. Capacity additions at Khavda outpaced the transmission infrastructure needed to evacuate electricity. When generation exceeds evacuation capacity, surplus power is effectively wasted.

The second component — Rs 800-1,000 crore — came from selling power below contracted Power Purchase Agreement (PPA) rates.

The context is important.

In FY26, the Inter-State Transmission System (ISTS) waiver, which exempted renewable projects commissioned before June 2025 from transmission charges for 25 years, was nearing expiry.

To lock in this long-term benefit, AGEL rushed to commission a disproportionate amount of capacity before the deadline. However, some of these projects became operational before their PPAs were activated. As a result, AGEL sold the electricity as “infirm power” in the merchant market, where prices were below contracted PPA tariffs.

Source: AGEL Q4 FY26 earnings call

In effect, AGEL gave up roughly 14% of FY26 EBITDA to capture 25 years of ISTS benefit on those plants. Management described the impact as “anomalous” and unlikely to recur. By Q4 FY26, additional transmission lines at Khavda had already become operational, while merchant pricing was higher than Q3. The cost was borne upfront. The benefit compounds over decades.

Balance sheet and debt

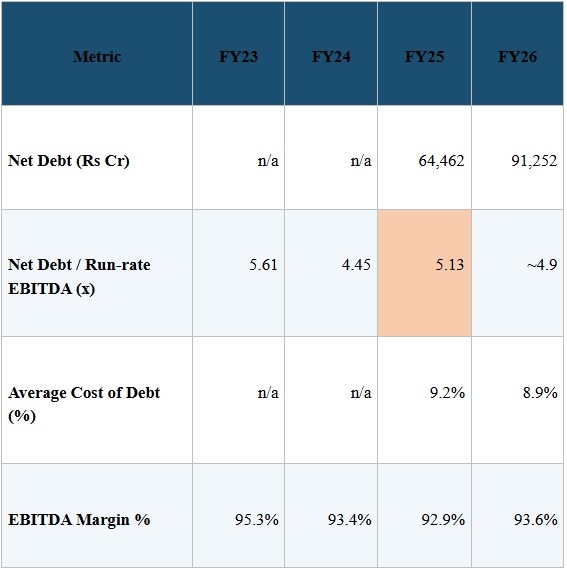

AGEL’s net debt rose from Rs 64,462 crore in March 2025 to Rs 91,252 crore in March 2026, an increase of Rs 26,790 crore in one year.

Source: AGEL FY25 Annual Report 5-year KPI table; AGEL Q4 FY26 IP slides

The number appears alarming, given that consolidated equity capital stands at Rs 19,965 crore. But the leverage ratio tells a more nuanced story.

Net debt to run rate EBITDA declined steadily from 6.66x in FY20 to 4.45x in FY24, then reversed in FY25 to 5.13x as capital expenditure outpaced cash generation. In FY26, it stabilised near 5x.

Meanwhile, the Japanese Credit Rating Agency assigned AGEL an inaugural BBB+ rating, equivalent to India’s sovereign credit rating. The cost of debt fell to 8.9% with downward pressure expected.

However, India Ratings has placed AGEL’s working capital facilities on Rating Watch with negative implications.

The bigger question is whether AGEL can fund the Rs 40,000–45,000 crore capex planned for FY27 without equity dilution. Internal accruals supported by a 91% EBITDA margin help, but they are unlikely to fully finance the scale of expansion AGEL is pursuing.

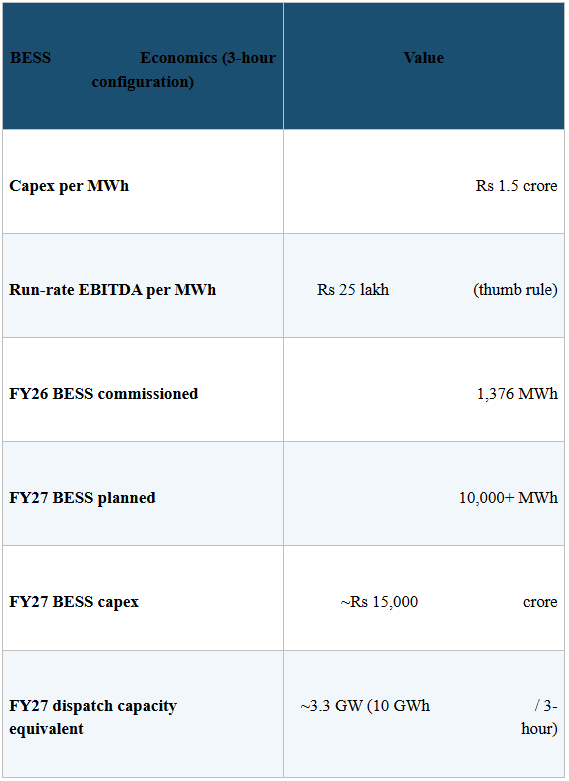

The battery bridge

AGEL added 1,376 MWh of Battery Energy Storage System (BESS) capacity at Khavda in FY26. Management says the site already represents roughly 50% of India’s installed BESS capacity.

The FY27 plan is to add more than 10 GWh.

Source: AGEL Q4 FY26 IP. Q4 FY26 earnings

Batteries solve three strategic problems for AGEL.

First, they hedge against curtailment that cost AGEL Rs 500 crore in FY26.

Second, they bridge the gap when transmission lags generation by absorbing daytime solar output and dispatching it during the evening peak.

Third, they offer EBITDA economics broadly equivalent to or slightly better than core renewables.

Valuation

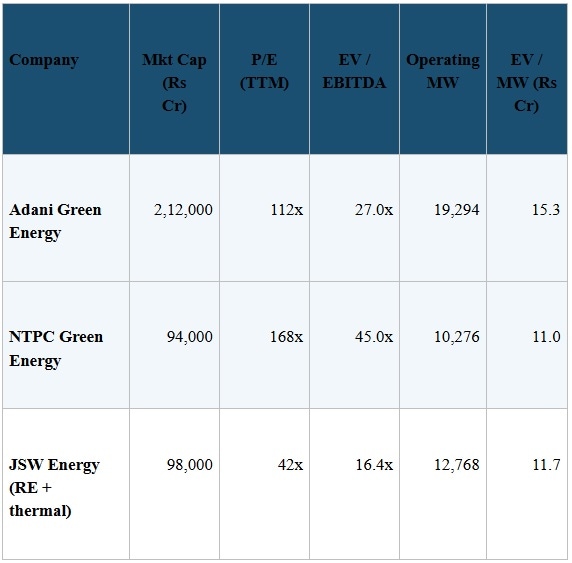

AGEL currently trades at Rs 1,290 per share, valuing the equity at Rs 2,12,000 crore. Trailing Price-to-Earnings (P/E) is 117x, and Enterprise Value to EBITDA (EV/EBITDA) is 27x.

Source: http://www.screener.in

AGEL trades at a discount to NTPC Green on EV/EBITDA, but at a significant premium to JSW Energy.

Part of that premium is justified by 100% renewable mix, scale, and a 91% EBITDA margin that JSW Energy cannot match.

At the same time, investors must account for several risks:

For investors, three variables matter most in FY27:

If AGEL delivers on all three, the market may begin valuing it as the central builder of India’s energy transition.

We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

In FY26, Adani Green Energy Limited (AGEL) added 5,051 megawatts (MW) of renewable energy capacity, the largest greenfield renewable addition by any company outside China.

During the same period, India added 55 gigawatts (GW), or 55,000 MW, of non-fossil fuel capacity, marking the country’s best year on record. This includes solar, wind, biomass, and both small and large hydro projects.

That means AGEL alone accounted for roughly 9% of India’s total renewable capacity additions and nearly 14% of the country’s solar and wind additions.

With India’s installed non-fossil base now at 283 GW and the official target set at 500 GW by 2030, the country must add another 50-55 GW annually over the next five years. AGEL is currently the single largest contributor to that expansion.

Source: http://www.tradingview.com

This explains why the stock has been rallying.

To understand AGEL’s long-term outlook, three questions matter:

The pace of green energy addition

AGEL ended FY26 with 19.3 GW of operating renewable capacity, up from 14.2 GW a year earlier. The 35% year-on-year growth extends a five-year capacity CAGR of 42%.

In terms of units of power sold, energy sales reached 37.6 billion units (BU), up 34% YoY, roughly equivalent, according to AGEL, to Denmark’s annual electricity consumption.

Source: AGEL FY25 Annual Report 5-year KPI table; AGEL Q4 FY26 Investor Presentation

However, the composition of that growth matters.

Of the 5,051 MW added in FY26, 4,613 MW came from a single site — Khavda. Another 438 MW came from Rajasthan, while Andhra Pradesh contributed the remainder.

In effect, one mega-project is driving the company’s growth trajectory, with every other site playing a supporting role.

The Khavda engine

Khavda, a 538-square-kilometre stretch of wasteland in the Rann of Kutch, had no operating capacity just two years ago.

Today, it hosts 9.4 GW of solar, wind, and hybrid projects, along with 1,376 megawatt-hours (MWh) of battery storage capacity. In FY26 alone, Khavda contributed 5.3 GW of AGEL’s total capacity addition. The target is 30GW by FY29.

Source: AGEL FY25 Annual Report; Investor presentations

AGEL’s execution strategy at Khavda rests on three pillars:

One detail often overlooked is that AGEL’s internal capability is 7-8 GW of capacity addition per year. Management is throttling delivery to 4.5-5 GW because the transmission grid downstream cannot evacuate any faster.

In FY27, another 14-15 GW of evacuation capacity is expected to come online at Khavda. If that lands on schedule, AGEL’s pace of execution could accelerate significantly. But scaling this quickly has unintended consequences.

In FY26, those consequences showed up as roughly Rs 1,500 crore of foregone EBITDA.

Why AGEL left Rs 1,500 crore voluntarily on the table

During its Q4 FY26 earnings call, AGEL disclosed that it sacrificed between Rs 1,200 crore and Rs 1,500 crore of EBITDA during the year.

The loss came from two sources.

First, around Rs 500 crore was lost due to grid curtailment. Capacity additions at Khavda outpaced the transmission infrastructure needed to evacuate electricity. When generation exceeds evacuation capacity, surplus power is effectively wasted.

The second component — Rs 800-1,000 crore — came from selling power below contracted Power Purchase Agreement (PPA) rates.

The context is important.

In FY26, the Inter-State Transmission System (ISTS) waiver, which exempted renewable projects commissioned before June 2025 from transmission charges for 25 years, was nearing expiry.

To lock in this long-term benefit, AGEL rushed to commission a disproportionate amount of capacity before the deadline. However, some of these projects became operational before their PPAs were activated. As a result, AGEL sold the electricity as “infirm power” in the merchant market, where prices were below contracted PPA tariffs.

Source: AGEL Q4 FY26 earnings call

In effect, AGEL gave up roughly 14% of FY26 EBITDA to capture 25 years of ISTS benefit on those plants. Management described the impact as “anomalous” and unlikely to recur. By Q4 FY26, additional transmission lines at Khavda had already become operational, while merchant pricing was higher than Q3. The cost was borne upfront. The benefit compounds over decades.

Balance sheet and debt

AGEL’s net debt rose from Rs 64,462 crore in March 2025 to Rs 91,252 crore in March 2026, an increase of Rs 26,790 crore in one year.

Source: AGEL FY25 Annual Report 5-year KPI table; AGEL Q4 FY26 IP slides

The number appears alarming, given that consolidated equity capital stands at Rs 19,965 crore. But the leverage ratio tells a more nuanced story.

Net debt to run rate EBITDA declined steadily from 6.66x in FY20 to 4.45x in FY24, then reversed in FY25 to 5.13x as capital expenditure outpaced cash generation. In FY26, it stabilised near 5x.

Meanwhile, the Japanese Credit Rating Agency assigned AGEL an inaugural BBB+ rating, equivalent to India’s sovereign credit rating. The cost of debt fell to 8.9% with downward pressure expected.

However, India Ratings has placed AGEL’s working capital facilities on Rating Watch with negative implications.

The bigger question is whether AGEL can fund the Rs 40,000–45,000 crore capex planned for FY27 without equity dilution. Internal accruals supported by a 91% EBITDA margin help, but they are unlikely to fully finance the scale of expansion AGEL is pursuing.

The battery bridge

AGEL added 1,376 MWh of Battery Energy Storage System (BESS) capacity at Khavda in FY26. Management says the site already represents roughly 50% of India’s installed BESS capacity.

The FY27 plan is to add more than 10 GWh.

Source: AGEL Q4 FY26 IP. Q4 FY26 earnings

Batteries solve three strategic problems for AGEL.

First, they hedge against curtailment that cost AGEL Rs 500 crore in FY26.

Second, they bridge the gap when transmission lags generation by absorbing daytime solar output and dispatching it during the evening peak.

Third, they offer EBITDA economics broadly equivalent to or slightly better than core renewables.

Valuation

AGEL currently trades at Rs 1,290 per share, valuing the equity at Rs 2,12,000 crore. Trailing Price-to-Earnings (P/E) is 117x, and Enterprise Value to EBITDA (EV/EBITDA) is 27x.

Source: http://www.screener.in

AGEL trades at a discount to NTPC Green on EV/EBITDA, but at a significant premium to JSW Energy.

Part of that premium is justified by 100% renewable mix, scale, and a 91% EBITDA margin that JSW Energy cannot match.

At the same time, investors must account for several risks:

For investors, three variables matter most in FY27:

If AGEL delivers on all three, the market may begin valuing it as the central builder of India’s energy transition.

We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Rahul Rao has helped conduct financial literacy programmes for over 1,50,000 investors. He has also worked at an AIF, focusing on small and mid-cap opportunities.

Disclosure: The writer or his dependents do not hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.